SMM May 11 News:

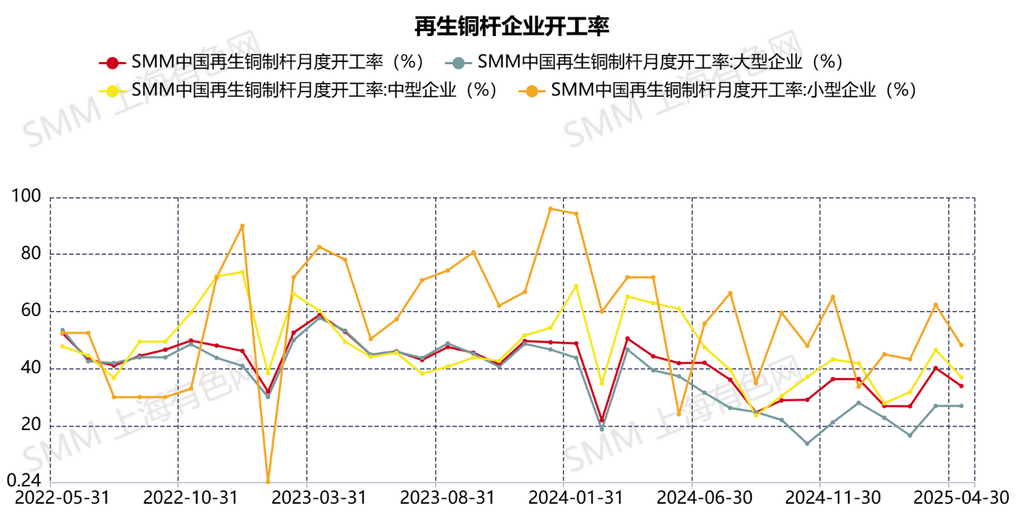

The operating rate of secondary copper rod production in April was 33.89%, lower than the expected 36.8%, representing a 6.29% MoM decrease and a 10.42% YoY decrease. Due to the escalating US-China trade war, the Customs Tariff Commission of the State Council announced on April 4, during the Qingming Festival holiday, that starting from 12:01 a.m. on April 10, 2025, a 34% tariff would be imposed on all imported goods originating from the US. This news triggered a sharp decline in copper market prices, with SHFE copper hitting the daily limit down and continuing to fall for three consecutive days post-holiday. The significant pullback in copper prices left secondary copper raw material suppliers uncertain about how to respond, prompting them to hold back cargoes and wait for copper prices to rebound. As the market gradually absorbed the impact of the tariff issues between China and the US, copper prices rebounded to around 78,000 yuan/mt. However, the inventory costs of secondary copper raw material suppliers, such as for bare bright copper with an acquisition price range of 73,000-74,000 yuan/mt, still left a nearly 1,000 yuan/mt gap between the market price of secondary copper raw materials and the suppliers' inventory costs, even after the copper price rebound. Consequently, secondary copper raw material suppliers stood firm on their quotes. Secondary copper rod enterprises reported that the availability of high-grade secondary copper raw materials in the market was extremely limited, with prices far exceeding normal and reasonable levels.

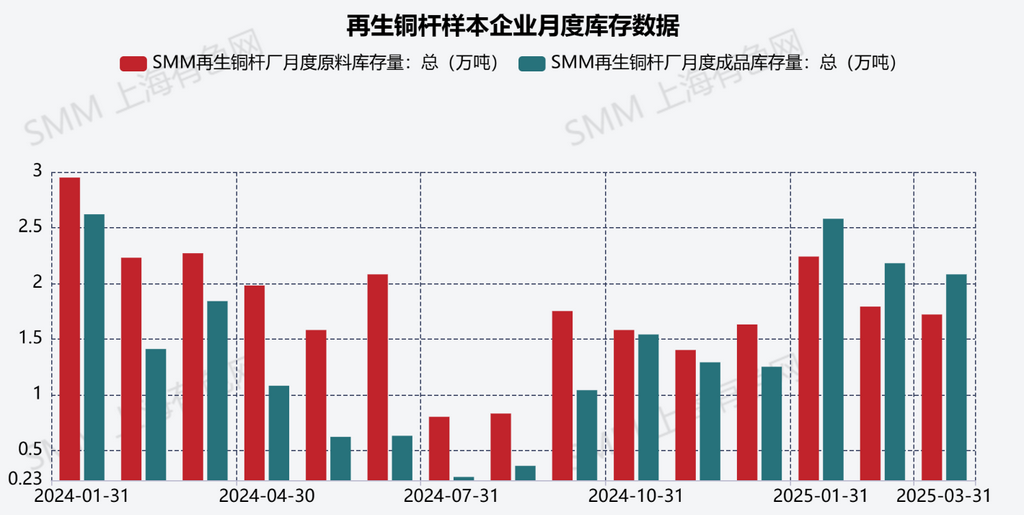

From the perspective of raw material inventory data, the raw material inventory of secondary copper rod enterprises in April was 16,000 mt, representing a 1,200 mt MoM decrease. Due to the reduced supply of high-grade secondary copper raw materials, many secondary copper rod enterprises were unable to procure sufficient raw materials and were forced to reduce their operating days. As a result, the operating rate of sampled secondary copper rod enterprises in April declined significantly. In terms of pricing, the average discount of secondary copper rod against copper futures in April was 139 yuan/mt, representing an 830 yuan/mt MoM narrowing. High raw material prices compelled secondary copper rod enterprises to raise their selling prices, leading to a 700 yuan/mt narrowing in the monthly average price difference between copper cathode rod and secondary copper rod to 780 yuan/mt. End-use consumption was almost entirely driven by rigid demand, with weak supply and demand contributing to a 5,900 mt decrease in finished product inventories of secondary copper rod enterprises to 14,900 mt.

In summary, under the circumstances of sharp fluctuations in copper prices driven by macro factors and the high prices and significantly reduced supply of secondary copper raw materials, the operating rate of secondary copper rod production declined markedly. Entering the off-season of consumption in May, the operating rate of secondary copper rod production is expected to continue to pull back to 32.74%.

The raw material inventory of secondary copper rod enterprises in April was 16,000 mt.

After the sharp decline in copper prices, the rebound was limited. The average inventory price level of secondary copper raw material suppliers was 73,000-74,000 yuan/mt, but after copper prices rebounded to 78,000 yuan/mt, they lacked further upward momentum, with the corresponding price of bare bright copper only reaching 72,000 yuan/mt. Therefore, secondary copper raw material suppliers were not in a hurry to sell their inventory of secondary copper raw materials. Additionally, due to the supply deficit in the secondary copper raw material market, the prices of secondary copper raw materials tended to follow increases but not decreases. Secondary copper rod enterprises reported that high raw material prices were continuously compressing their sales profits, with some trading days even experiencing varying degrees of losses.Therefore, secondary copper rod enterprises produce based on sales and do not prepare excessive inventory of secondary copper raw materials.

The operating rate of secondary copper rod production is expected to be 32.74% in May.

In May, as Sino-US trade relations eased, although copper prices stabilized at 78,000 yuan/mt, there was still a certain gap from the inventory cost of suppliers holding secondary copper raw materials. Additionally, entering the traditional consumption off-season, end-use demand weakened. Coupled with the continuous lack of recovery in the supply of secondary copper raw materials, it will be difficult for the operating rate of secondary copper rod enterprises to improve.